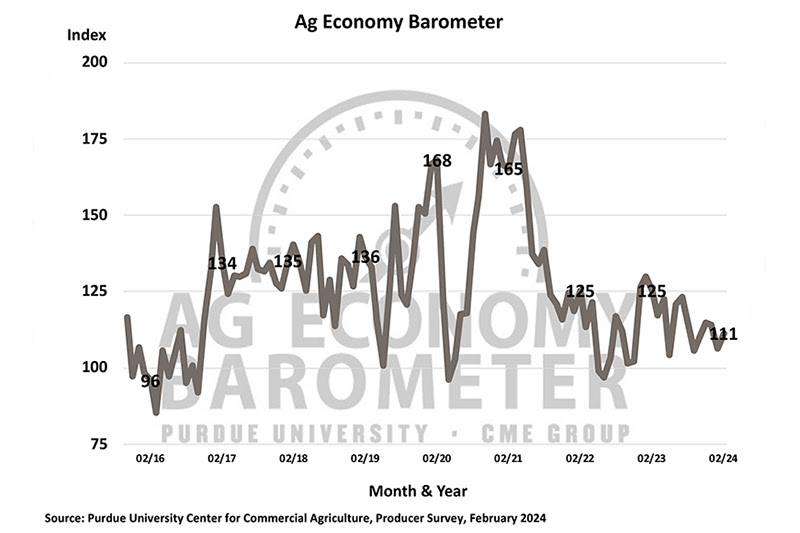

INDIANA — The latest Purdue University/CME Group Ag Economy Barometer reveals a modest increase in farmer sentiment compared to the previous month. However, concerns remain regarding farm financial performance in the year ahead.

The February barometer reading reached 111, marking a 5-point rise from last month. The slight uptick is attributed to producers expressing increased optimism about the future, with the Future Expectations Index climbing 7 points to 115. However, the Current Conditions Index remained unchanged. Farmers’ financial performance expectations did not keep pace despite their improved outlook for the future. February’s Farm Financial Performance Index registered at 85, a slight dip from January and notably lower than its recent peak in December. The February survey was conducted from Feb. 12-16.

“Weak crop prices continue to weigh heavily on financial expectations, with mid-February Eastern Corn Belt cash prices for corn and soybeans declining by 7% and 8%, respectively, compared to two months earlier,” said James Mintert, the barometer’s principal investigator and director of Purdue University’s Center for Commercial Agriculture.

When producers were asked about their primary concerns for farm operations in the upcoming year, the top concern cited by 34% of respondents was “high input costs,” closely followed by “lower crop/livestock prices,” chosen by 28% of respondents. Worries about rising interest rates among producers seem to have diminished somewhat, with only 18% of February respondents citing it as a top concern, down from 26% who did so in November.

The Farm Capital Investment Index remains weak at 34 points, 9 points lower than last year. Producers reluctant to make significant investments highlighted concerns over high production costs and weak output prices. The percentage of farmers worried about farm profitability has tripled since last October. This month, 22 out of every 100 farmers pointed to farm profitability concerns, while previously, only 7 out of every 100 farmers felt the same way.

The Short-Term Farmland Values Expectations Index held steady compared to January but declined by 4 points from a year ago and by 30 points from two years ago. Although the farmland index remains positive, it is clear that overall sentiment regarding future increases in farmland values is weaker than it was a couple of years ago. Among producers who expect values to increase next year, demand from non-farm investors is the top reason cited for their optimism.

Each February, the barometer survey asks producers about growth plans for their farm operations in the upcoming five years. This year, 4 out of 10 respondents expressed no plans for growth, with 14% saying they plan to exit or retire. Alternatively, just over 3 out of 10 respondents anticipate their farm’s annual growth rate to exceed 5%. Responses to this question, consistent in recent years, point to further consolidation among farm operations.

“To put growth rates into perspective, consider that a farm growing at a 5% annual rate will double in size in about 14 years, whereas a farm growing at an annual rate of 10% will need just seven years to double,” Mintert said.

Interest in leasing farmland for solar energy development remains strong, with 10% of respondents discussing such projects in the last six months. Rates varied widely, but over half of the respondents reported being offered lease rates of $1,000 per acre or more. The top end for solar lease rates appears to be rising over time. When this question was posed in June 2021, just 27% of respondents reported a lease rate offer of $1,000 or more per acre, compared to 56% of respondents this year.